2017 - 2018:

2018 - 2019:

2014 - 2015:

2015 - 2016:

2016 - 2017:

{kind=link}

2019 - 2020:

Assets

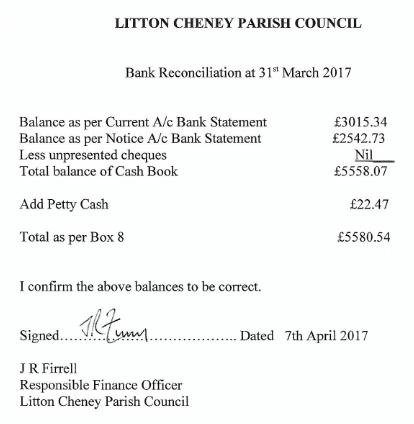

Finance 2019-2020

Policy

Parish Council business is governed by a set of formal documents - click on a title to view:

Copies of documents satisfying the Transparency Code can be accessed by clicking on the appropriate link:

Litton Cheney Parish Council Documentation

Created January 2017

Reviewed February 2019

Next review February 2020

Information Title

Information which should be published

Date Published

Location

All items of expenditure

above £100

Annual publication no later than 1 July in the year immediately

following the accounting year to which it relates

Publish details of each individual item of expenditure

Copies of all books, deeds, contracts, bills, vouchers, receipts and

other related documents do not need to be published but should

remain available for inspection. For each individual item of

expenditure the following information must be published:

a. date the expenditure was incurred,

b. summary of the purpose of the expenditure,

c. amount

d. Value Added Tax that cannot be recovered.

In Minutes of bi-

monthly meetings

Village Website

Records with Parish

Clerk

Minutes

Minutes

Minutes

All VAT is generally

recoverable

Annual Return &

Governance Statement

End of Year Accounts

Internal Audit

External Audit (if applicable)

Annual publication no later than 1 July in the year immediately

following the accounting year to which it relates.

Publish signed statement of accounts according to the format

included in the Annual Return form. It should be accompanied by:

a. copy of the bank reconciliation for the relevant financial year,

b. an explanation of any significant variances (e.g. more than 10-15

percent) in the statement of accounts for the relevant and previous

year,

c. an explanation of any differences between ‘balances carried

forward’ and ‘total cash and short term investments’, if applicable.

May of each year

post Annual Meeting

Post External

Audit - September

Website

List of Councillors or Member

Responsibilities

Annual publication of councillor or member responsibilities within 14

days of the Annual Meeting in May immediately following the

accounting year to which it relates, including:

a. names of all councillors or members,

b. committee or board membership and function (if Chairman or

Vice-Chairman),

c. representation on external local public bodies (if nominated to

represent the authority or board).

May of each year

Website

Model Publications

Scheme

Location of Public Land and

Building Assets

Annual publication no later than 1 July in the year immediately

following the accounting year to which it relates.

Parish councils are to publish details of all public land and building

assets - either in its full asset and liabilities register or as a village

inventory.

The following information must be published:

a. description (what it is, including size/acreage),

b. location (address or description of location),

c. owner / custodian, e.g. the authority manages the land or asset on

behalf of a local charity.

d. date of acquisition (if known),

e. cost of acquisition (or proxy value),

f. present use.

April each year,

following Inventory

Review

Village Inventory and

Website

Minutes, Agendas and

Papers of Formal Meetings

Publication of draft minutes from all formal meetings not later than

one month after the meeting has taken place.

Publication of meeting agendas and associated meeting papers not

later than three clear days before the meeting to which they relate is

taking place

As directed

Website & Main

Village Notice Board

Litton Cheney Parish Council Transparency Checklist

In December 2014 the Department for Communities and Local Government (DCLG) published the Local Audit and Accountability

Act 2014 for Smaller Authorities. The Code is a requirement for smaller authorities to make information available for local people to

increase democratic accountability.

Transparency gives local people the tools and information they need to hold local public bodies to account, setting out a new audit

framework for local public authorities which are currently covered by the Audit Commission regime. Under the new audit framework

parish councils with an annual turnover not exceeding £25,000 will be exempt from routine external audit. In place of routine audit,

these smaller authorities will be subject to the new transparency requirements laid out in this Code. This will enable local electors

and ratepayers to access relevant information about the authorities’ accounts and governance.The full document can be viewed

here: Transparency Code for Smaller Authorities

Transparency Code for Smaller Authorities

PARISH COUNCIL ADMINISTRATION

Village Information v

Local Amenities v

Village Amenities v

About Litton Cheney v

Dorset Council v

Parish Council v